Highlights ZimCal’s Goal Over Three Consecutive Proxy Contests – A Debt Buyout at Above Market Price – and Misaligned Incentives

Reveals Distortions in ZimCal’s Campaign About Key Issues

Highlights Concerning Lack of Relevant Experience Among ZimCal Nominees, Including Eric Kelly’s History of Near-Complete Value Destruction and Lawsuit Alleging Fraud, Financial Improprieties and Whistleblower Retaliation

Urges Shareholders to Again Support Medallion’s Proven Leadership and Success By Voting the WHITE Proxy Card FOR ONLY Medallion’s Nominees

NEW YORK, June 04, 2026 (GLOBE NEWSWIRE) -- Medallion Financial Corp. (NASDAQ: MFIN) (“Medallion” or the “Company”), today issued the following response to distortionary claims made by Stephen Hodges and his affiliates (collectively “ZimCal”), in the last days of his desperate third consecutive proxy contest against the Company. Medallion also highlighted the lack of relevant experience in ZimCal’s nominees, including the concerning business track record of nominee Eric Kelly.

Mr. Hodges previously stated in February 2024 that the Company would face a proxy contest “every year” if it refused to buyout his debt on his terms. Shareholders saw through his distortions last time and overwhelmingly supported management in a landslide, and we urge you once again to look past ZimCal’s distortions and vote for Medallion’s highly qualified Board on the WHITE proxy card.

WHO IS STEPHEN HODGES, THE FOUNDER OF A CREDIT FUND WITH NO DISCLOSED AUM, NO LISTED EMPLOYEES, AND NO DISCLOSED PHYSICAL OFFICE?

Before evaluating Mr. Hodges’ grievances, shareholders should understand the profile of the man seeking to capture three of eight board seats, ~38% of the board, destroy the Board’s strong track record of success, and replace key members of the Board, including our co-founder, chair of the Nominating and Governance Committee, and the former CEO of a public specialty finance company and a regional bank.

Just like the 2024 contest, Mr. Hodges IS buying up shares to acquire votes and is falsely portraying himself as aligned with other investors. Mr. Hodges and his affiliates first acquired shares in December 2023 shortly before nominating directors at the 2024 annual meeting. He rapidly accumulated a 70,000-share stake before the meeting, then liquidated nearly the entire position after losing the election. In December 2025, when he nominated directors for this upcoming meeting, he beneficially owned only 3,010 shares, or 0.01% of outstanding shares. In the five months since, he has acquired a 2.1% stake (only 0.8% of which was acquired before the record date and is entitled to vote at the election) to bolster the optics of his campaign, not because he believes in Medallion’s future. If he runs the same playbook as 2024, he will almost certainly sell those shares shortly after the June 9 meeting.

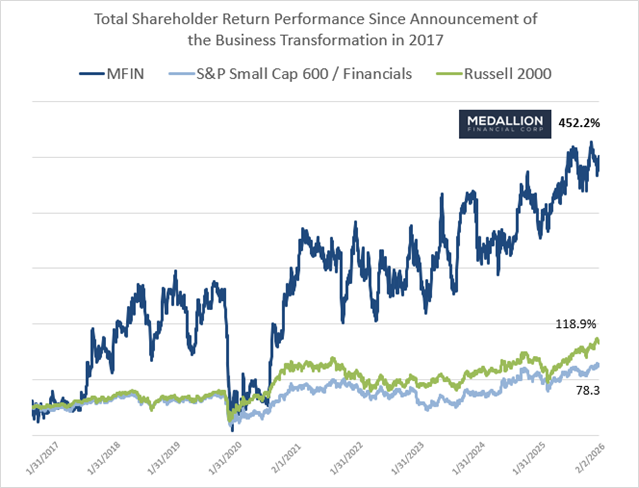

He is primarily a debt holder, not an equity investor. Mr. Hodges’ primary position in Medallion consists of illiquid trust preferred securities purchased at a steep discount in 2021. These are subordinated debt instruments that do not participate in equity upside, and currently pay him 6%, well below market for a security like this. While Medallion’s shareholders have earned a 452% total return since the Company’s transformation began, Mr. Hodges’ debt position has remained static.

Mr. Hodges has sought a repurchase or other liquidity solution for his distressed debt holdings for three years. His campaign is not about creating shareholder value. It is about pressuring Medallion to buy out his debt at a premium. He has demanded a buyout at more than double his purchase price (approximately 45 cents on the dollar, or $6.5 million). As late as April 13, 2026, Mr. Hodges proposed a debt-for-equity swap that would greatly dilute existing shareholders.

This is the third proxy campaign Mr. Hodges has launched in three years, making good on the threat he issued to the Company in 2024. In February 2024, Mr. Hodges threatened that if the Company did not agree to a settlement with him, including two variations on a debt buyout, he would run a proxy contest in 2024 and “every year thereafter if unsuccessful.” This campaign is his third since that threat. In 2024, shareholders rejected his nominees by a margin of 3.5 to 1. In 2025, after threatening to run a campaign, he withdrew his nominees at the last minute. He is back again. Shareholders should ask themselves: is this the behavior of a long-term value investor, or the signs of a self-interested fund pressing its agenda at the expense of the Company and all shareholders?

NOW, TO HIS CLAIMS:

CLAIM 1: Medallion’s performance has been declining

THE TRUTH:

Medallion has achieved consistent and long-term performance.

The Company’s Q1 results reflect strong loan growth that required the Company to book expected lifetime credit reserves upfront under CECL in the quarter the loans are originated (a well-known dynamic often called the ‘growth penalty’). These reserves will be earned back as the portfolio seasons and generates income in future periods. Gains from Medallion Capital are inherently volatile and can vary significantly from one quarter to the next, with no gains in Q1 but expectations for contributions in future periods.

Cherry-picking a single quarter, and portraying it as a downward trend, may be appropriate for a short-term trader like Mr. Hodges, who acquired 99.4% of his shares this year. But it does not tell the story that longer term holders have experienced:

- Net income over the last five years totals $266 million, exceeding the combined net income of Medallion’s first 25 years as a public company.

- Book value per share has risen 53% since 2021, from $11.40 to $17.53.

- Net Interest Income has grown at a 14.1% compound annual rate since 2021.

- The Company has returned over $68.5 million to shareholders through dividends and buybacks since 2022.

- The quarterly dividend has been raised by 75% since 2022.

Northland Capital Markets calls this “consistent execution across the company’s business lines.”

This performance also reflects consistent value creation for long-term shareholders who have invested with the Company for more than four months, and plan to remain invested with the Company. We urge those shareholders to disregard the short-term, self-interested analysis of a short-term trader like Mr. Hodges.

CLAIM 2: Medallion’s total shareholder return is the lowest in its peer group

THE TRUTH:

This is selective and deliberately false. Medallion’s total shareholder return since the beginning of its strategic transformation is 452%, and its total shareholder return has significantly outperformed its proxy peer group over 1-, 3-, and 5-year periods, based on a true unaffected date (when Mr. Hodges issued his first attack press release after nominating directors). Mr. Hodges extends the measurement period through May 1, 2026 to manufacture a negative comparison.

Source: FactSet. Based on starting date Jan. 31, 2017 and ending date Feb. 2, 2026 (unaffected date. 1-day before ZimCal’s public letter dated Feb. 3, 2026).

Jan. 31, 2017 starting date based on Medallion’s press release regarding the transformation plan: https://www.medallion.com/pdf/news_press_releases/press_release_17-01-31.pdf

CLAIM 3: ZimCal has nominated three candidates who fill gaps in the Board

THE TRUTH:

The Board of Directors unanimously concluded that the ZimCal nominees are materially unqualified to serve on the board of a regulated consumer lending institution and that their election would introduce regulatory risk and operational disruption at precisely the moment Medallion’s momentum is strongest.

The Company urges shareholders to carefully consider the following in evaluating ZimCal’s nominees:

Eric Kelly’s Business Track Record is Limited to Technology Hardware, With a History of Self-Dealing and Near-Complete Value Destruction

An overview of Mr. Kelly’s history reveals a startling track record of value destruction and self-dealing. These concerns are in addition to the allegations of financial improprieties by Mr. Kelly in a pending lawsuit, discussed below.

While Board Chairman for Sphere 3D Corporation, Mr. Kelly facilitated a merger with Overland Storage, where he was then serving as CEO. After he was named CEO of the combined company in 2014, his tenure was marked by significant losses, credit defaults, and financial engineering and self-dealing with his own entity, Silicon Valley Technology Partners, to avoid bankruptcy.1 In November 2018, Mr. Kelly facilitated a spinoff of Overland Storage to his affiliate Silicon Valley Technology Partners and other investors, and he departed as CEO of Sphere 3D with a total shareholder return of -99% during his tenure. His tenure at Overland Storage did not fare better, with the company liquidating in 2025.

More recently, Mr. Kelly joined the Sabre Corporation board in January 2025. As of June 1, 2026, Sabre’s total shareholder return has declined by 48%.

Mr. Kelly’s entire career has focused on technology hardware while seemingly tainted by an inability to create shareholder value and self-dealing. These deficiencies aside, Mr. Kelly has no background in consumer lending, specialty finance, bank regulation, or credit risk management. The Company believes this combination of a troubling track record and a complete absence of relevant expertise makes Mr. Kelly wholly unfit to serve as a director of a federally regulated bank holding company.

John Kiernan and Timothy Shanahan Lack Relevant Expertise that Would be Additive to the Medallion Board

ZimCal’s other two nominees were recycled from its withdrawn campaign in 2025 and they possess no relevant experience.

Mr. Kiernan’s professional background is centered on agriculture: he currently leads a Florida-based agribusiness and land management company. ZimCal points to a prior community bank board appointment as evidence of financial credentials, but that short-term stint was an activist-driven engagement that ended when the institution was acquired. He has no meaningful, current experience in consumer finance or bank regulation.

Timothy Shanahan is a restructuring advisor who has never served on a public company board. While his career has focused primarily on distressed, turnaround, and restructuring situations, his expertise would not be of value to Medallion as a profitable, growing, high-performing company operating in a complex regulatory environment. The Board is not in need of a restructuring expert – it needs directors who can oversee continued growth.

_______________

1 Overland Storage survives another day in the Last Chance Saloon (Nov. 6, 2018)

CLAIM 4: Medallion and its then President settled the SEC matter paying penalties

THE TRUTH:

First, the underlying allegations in the SEC matter related to conduct from 2014 through 2017, a decade ago. The Company and its leadership have operated transparently, grown Medallion Bank into one of the most profitable banks in the country by key metrics, and delivered record financial performance in the years since. Mr. Hodges is asking shareholders to judge a decade of exceptional performance by decade-old allegations that were never even proven.

Second, Mr. Hodges fundamentally misrepresents the SEC matter. The Company was never found guilty, nor did it admit to any wrongdoing.

Third, the matter is fully resolved. The Company and its CEO cooperated, reached a settlement, and moved forward, having determined that it was in the shareholders’ best financial interest to put this matter behind them.

Last, Mr. Hodges’ approach to the unproven allegations against the Company are strikingly different than he applies to the unproven allegations against Eric Kelly, one of his nominees. Mr. Kelly is the defendant in a pending lawsuit that is scheduled to go to trial in December 2026 brought by the former Chief Financial Officer of OT Global Protection (“OT Global”), where Mr. Kelly then served as CEO.

The complaint alleges that Mr. Kelly’s misconduct included:

- Alleged diversion of revenue for personal benefit: According to the complaint, customer revenue collected by Overland was directed by Mr. Kelly to his and his partner’s shared entity, rather than to Overland and its shareholders. The complaint alleges Mr. Kelly kept the financial statements of the two entities artificially separate, in violation of US GAAP, specifically to prevent Overland’s investors and debtors from learning about the revenue.

- Alleged misappropriation of customer prepayments: The complaint alleges that more than 10% of customer prepayments totaling tens of millions of dollars were distributed personally to Mr. Kelly and his partner. The distribution occurred without evidence of board approval, without disclosure to the CFO, and in violation of the requirement to hold the funds as restricted cash. Mr. Kelly allegedly insisted on being the sole person with signature authority over the accounts, even after the CFO advised that this was a fundamental violation of internal controls.

- Alleged tax fraud and manipulation of financial statements: The complaint alleges Mr. Kelly repeatedly changed factual representations about OT Global’s inventory risk. Mr. Kelly purportedly claimed 0% inventory risk to customers justifying his charging and collection of millions of dollars in reimbursements from them, while improperly claiming 100% risk to the government to receive tax deductions for the decrease in inventory value. According to the allegations, when the CFO raised concerns about Mr. Kelly’s likely violations of the tax code for prohibiting the accounting group from booking adjustments for inventory, he allegedly responded: “I have to certify and sign off on the numbers and the numbers will be my numbers, not accounting numbers.”

- Alleged termination of a whistleblower within two hours of submitting a complaint: On February 16, 2022, after months of raising concerns internally, the CFO sent a formal letter to the OT Global Board of Directors documenting Mr. Kelly’s alleged GAAP violations, IRS code violations, misrepresentations to customers, and improper revenue diversion. According to the complaint, less than two hours after that letter was delivered to the board, Mr. Kelly terminated his employment.

When asked about this lawsuit, Mr. Hodges’ counsel stated: “one former employee’s four-year old lawsuit against several defendants that has not proceeded beyond the pleadings stage is hardly material information.” Shareholders should be aware that Mr. Hodges wants to judge unproven allegations differently based on whether they are made against his own nominees.

CLAIM 5: The SBA declared an event of default of a subsidiary’s debentures

THE TRUTH:

This was a technical matter related to SBA rules and not a financial default. It did not arise from any criticism by the SBA of the subsidiary’s credit performance or concerns about the Company’s ability to meet its financial obligations. The Company has addressed this matter directly in its public filings, has received positive feedback from the SBA regarding the cure of such default2, and believes it will be resolved imminently.

CLAIM 6: ZimCal has engaged with Medallion over 50 times and been ignored or dismissed nearly every time

THE TRUTH:

Medallion has invested an enormous amount of time involving dozens of meetings and correspondence with Mr. Hodges and always engaged in good faith, as we would with any investor. In late 2023, the Company discussed offering to purchase Mr. Hodges’ trust preferred securities at a fair price. He rejected it and demanded a premium that would have transferred millions of dollars of value from common shareholders to him personally. When the Company declined, he chose to go public. That is not constructive engagement, but an attempt to create leverage. In his subsequent interactions with us, he has simply reiterated the same complaints about the Company’s value, none of which have been vindicated, and demanded that the Company change its practices and acquire his debt.

_______________

2 MEDALLION FINANCIAL CORP 8-K 2026-06-03

CLAIM 7: A board that has not held management accountable — citing director ages and tenure

THE TRUTH:

The Board standing for election includes John Everets, a former bank Chairman and CEO who led a successful $135 million institutional sale; Cynthia Hallenbeck, a former CFO of Citigroup’s treasury department; and Alvin Murstein, one of the founders of the Company of the strategic transformation that created over $266 million in net income over five years. These are not placeholder directors — they are the leaders who built this Company and delivered its historic transformation.

Director tenure is not a liability when the directors are the ones who executed a historic transformation.

THE BOTTOM LINE

Stephen Hodges is, at best, a would-be distressed debt speculator, purporting to manage a fund of undisclosed size, with an undisclosed number of employees, who bought a deeply subordinated instrument in 2021 and has spent the years since demanding that Medallion’s common shareholders subsidize his exit at a premium.

He is not a builder. He is not a long-term investor. He is someone who made a bet on illiquid paper, watched the equity he passed on generate 452% returns, and decided the response was to wage annual proxy warfare every year until someone writes him a check.

Shareholders have seen this before. In 2024, they rejected his nominees 3.5 to 1. His claims were wrong then and are wrong now. The Company’s results, independent equity research, and the institutional investors who just provided Medallion with a $75 million senior notes financing (rated A- by Egan-Jones), led by JP Morgan Investment Management, all point in the same direction.

Additionally, Medallion's Board has demonstrated a track record of responsiveness to shareholder feedback and commitment to thoughtful and deliberate refreshment. Five independent directors have been added over the past nine years, including three in the last six years alone, and the Company has a track record of engaging and reaching constructive outcomes with investors who criticize it.

The Nominating and Governance Committee approached the ZimCal nominees with that same open mind, individually reviewing and interviewing each of the three candidates. What the Committee found, however, was not a slate of constructive nominees who could provide valuable insight and relevant expertise, but a collection of mismatched backgrounds: a technology hardware executive whose last company was liquidated amid alleged misconduct, an agriculture company executive, and a restructuring advisor who has never served on a public company board. None of the nominees have the finance, lending, or regulatory expertise this Company requires at this stage of its growth.

Medallion urges all shareholders of record as of April 13, 2026 to vote the WHITE universal proxy card FOR John Everets, Cynthia A. Hallenbeck, and Alvin Murstein — the directors who built this Company and are continuing to build it.

For more information visit www.votemedallion.com or call Alliance Advisors toll-free at (844) 202-5720.

About Medallion Financial Corp.

Medallion Financial Corp. (NASDAQ: MFIN) and its subsidiaries originate and service a portfolio of consumer loans and mezzanine loans in various industries. Key industries served include recreation (towable RVs and marine) and home improvement (replacement roofs, swimming pools, and windows). Medallion Financial Corp. is headquartered in New York City, NY, and its largest subsidiary, Medallion Bank, is headquartered in Salt Lake City, Utah.

Important Additional Information and Where to Find It

Medallion has filed its definitive proxy statement, accompanying WHITE universal proxy card and other relevant documents with the Securities and Exchange Commission (“SEC”) in connection with the solicitation of proxies for Medallion’s upcoming 2026 Annual Meeting of Shareholders. BEFORE MAKING ANY VOTING DECISION, SHAREHOLDERS OF THE COMPANY ARE URGED TO READ ALL RELEVANT DOCUMENTS FILED WITH OR FURNISHED TO THE SEC, INCLUDING MEDALLION’S DEFINITIVE PROXY STATEMENT AND ANY AMENDMENTS AND SUPPLEMENTS THERETO, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. Investors and shareholders will be able to obtain a copy of the definitive proxy statement and other documents filed by the Company with the SEC free of charge from the SEC’s website at www.sec.gov. In addition, copies will be available at no charge by visiting the “Investor Relations” section of Medallion’s website at www.medallion.com, as soon as reasonably practicable after such materials are filed with, or furnished to, the SEC.

Investor Relations: InvestorRelations@medallion.com | 212-328-2176

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/50beda21-3336-4d84-aec7-c135a47338d4

![]()